Beyond Conventional Wisdom

Emerging markets carry a persistent reputation: that of economies dependent on a dirty energy mix, largely dominated by coal and hydrocarbons. Under this view, the energy transition is seen as a luxury for developed countries. Emerging economies would supposedly get there later, once their development cycle is complete.

The facts tell a very different story. Among the world’s ten greenest electricity mixes, four belong to emerging or developing countries, with Brazil and Chile exceeding 90% renewable share. The shift is not a future prospect; it is already underway.

More importantly, emerging economies are now the focal point of global energy growth. In 2024, 80% of the growth in global energy demand came from emerging markets, with India alone surpassing the entire group of advanced economies. These countries are developing a wide range of energy sectors, from solar and wind power to biofuels and biomethane, that combine the energy transition, energy independence, and the utilization of local resources. They are the ones reshaping the geography of the transition.

Against this backdrop, a question naturally arises for investors: beyond conventional wisdom, where do the real opportunities offered by the energy transition in emerging markets actually lie?

Clean Energy Investment Now Surpasses Fossil Fuels

The first strong signal is the tipping point reached in capital expenditure. In 2024, clean energy investment in emerging markets reached USD 1 trillion, now representing nearly twice the level of spending on fossil fuels. This crossover, visible since 2021, has accelerated dramatically: renewable energy capex nearly doubled between 2019 and 2024, while fossil fuels stagnated.

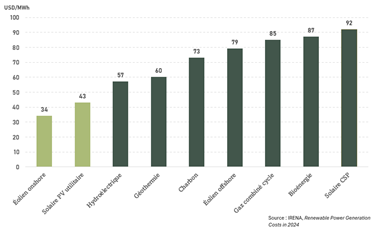

This momentum is all the more significant given that it is accompanied by a decisive economic advantage: the cost of renewable energy is structurally lower than that of fossil fuels on a global scale. The global average LCOE (levelized cost of electricity over the lifetime of an installation) stands at around USD 43/MWh for solar and USD 34/MWh for onshore wind, compared with USD 73/MWh for coal. This price competitiveness makes renewable projects economically rational, regardless of any ESG regulatory constraints.

Emerging Markets Already Well Positioned in Renewables

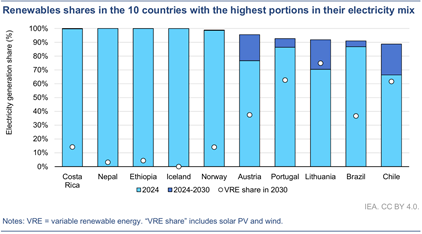

This investment momentum is already reflected in the structure of the electricity systems of many emerging markets. Contrary to certain preconceptions, several of them already have an electricity mix largely dominated by renewable energy. Costa Rica, Nepal, and Ethiopia boast an almost entirely renewable electricity mix (close to 100%), rivaling developed countries such as Iceland or Norway. Brazil and Chile, two heavyweights of the emerging market universe, are set to exceed 90% renewable share in their electricity mix by 2030.

Source: IEA Renewables 2025 report

The case of Brazil is emblematic: as the world’s seventh-largest electricity market, the country produced 88% of its electricity from renewable sources in 2024, and its overall energy mix reached 50% renewable. Between 2014 and 2024, the share of wind and solar increased fifteenfold, rising from 2% to 24% of electricity generation, enabling a 45% reduction in fossil-fuel-based generation over the same period.

China, although often associated with its coal-fired power plants, accounts for nearly 60% of global growth in renewable capacity and is expected to meet its 2035 wind and solar target five years ahead of schedule, having installed more solar capacity in 2024 than the rest of the world combined.

These existing achievements are only a starting point. The Middle East and North Africa (MENA) region recorded the largest upward revision (+25%) to its renewable deployment forecasts for 2025-2030, driven by the rise of solar PV in Saudi Arabia, while ASEAN benefits from a +15% upward revision thanks to more ambitious auction policies. Concretely, the MENA region is expected to add 62 GW of renewable capacity over this period, of which more than 85% will come from solar PV. Installed solar capacity, which stood at around 24 GW at the end of 2024, could exceed 180 GW by 2030 according to MESIA (the Middle East Solar Industry Association). Saudi Arabia, which is targeting 50% renewable in its electricity mix by 2030, alone accounts for more than a third of this growth.

Furthermore, the IEA’s World Energy Outlook 2025 projects that renewable capacity additions in emerging markets will exceed 600 GW per year on average by 2035, roughly four times France’s total electricity capacity each year.

This acceleration stands in stark contrast to the trajectory of certain advanced economies. The IEA has revised its renewable capacity forecast for the United States over 2025-2030 downward by nearly 50%, due to the early elimination of federal tax credits, new import restrictions, and the suspension of offshore wind permits. In the United Kingdom, delays on offshore wind have created a shortfall estimated at 32 GW relative to 2030 targets. In South Korea, the 11th Basic Plan for Electricity, finalized in February 2025 under the Yoon administration, lowered the renewable target to 22% for 2030, below the 30% enshrined in the country’s Nationally Determined Contributions, while also failing to meet the COP28 commitment to triple installed renewable capacity by 2030.

India: The driver of Renewable Growth in Asia-Pacific

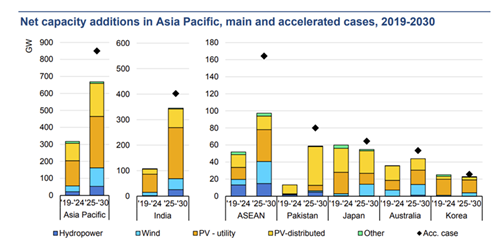

Among the emerging economies engaged in this energy transformation, India holds a distinctive position. According to the IEA, installed capacity is expected to nearly double between 2025 and 2030 in Asia-Pacific. India alone accounts for more than half of this expansion, with 250 GW of installed renewable capacity by year-end 2025 and a target of 500 GW of non-fossil capacity by 2030.

Source: IEA Renewables 2025 report

This momentum is in line with India’s massive investment plan: USD 13.3 billion in 2024 (+40% year-on-year) to diversify its energy mix. Utility-scale and distributed solar PV dominate capacity additions, followed by wind, which is also experiencing a strong rebound.

The results are already tangible: India reached the 50% non-fossil installed capacity threshold in June 2025, more than five years ahead of its NDC target under the Paris Agreement, establishing itself as one of the most dynamic players in the renewable transition among emerging markets.

Greenko, one of India’s leading renewable energy producers and a benchmark bond issuer in the emerging markets universe, perfectly illustrates this momentum. Founded in 2004, the company has grown its installed capacity from approximately 2.5 GW in 2018 to more than 11 GW today, spread across 14 Indian states through a wind, solar, and hydroelectric mix, with an ambition of 50 GW by 2030, which would make it one of the largest renewable energy producers in the world.

Biofuels: Energy Security and a Growth Driver

Beyond the decarbonization of the electricity sector, biofuels represent an often-underestimated opportunity for emerging markets. Their value is twofold: they contribute to reducing CO2 emissions in the transport sector while also reducing dependence on oil imports, a critical issue in the current geopolitical context.

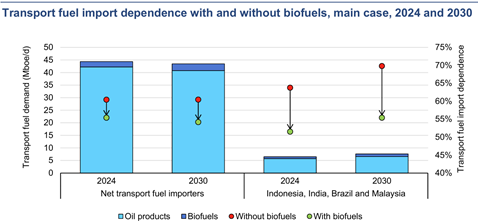

Persistent tensions in the Middle East, and particularly around Iran, are a reminder of the vulnerability of oil supply chains. For countries such as India, Indonesia, or Brazil, which are heavily dependent on transport fuel imports, the development of biofuels offers a tangible lever for energy sovereignty. IEA data show that the integration of biofuels can significantly reduce these countries’ dependence ratio on transport fuel imports.

Source: IEA Renewables 2025 report

In Brazil, FS Bioenergia embodies this same movement. As the country’s fourth-largest ethanol producer, with a capacity of 2.2 billion liters per year, the company is a pioneer in the production of corn ethanol, a technology that is more cost-competitive and has a lower carbon footprint than the dominant sugarcane sector. It benefits directly from Brazil’s Combustível do Futuro program, a law adopted in 2024 that provides for raising the ethanol blend rate in gasoline from 22% to 35% by 2030, structurally supporting demand.

Biogas and Biomethane: A Potential Concentrated in Emerging Markets

Another area of opportunity deserves attention: biogas and biomethane. According to the IEA report published in 2025, nearly 1,000 billion cubic meters of natural gas equivalent could be produced sustainably each year from existing organic waste streams, equivalent to a quarter of global natural gas demand. 80% of this potential is concentrated in emerging and developing economies, led by Brazil, China, and India, India’s biogas production potential exceeds its current natural gas consumption, while the country today exploits less than 5% of this resource.

Emerging Asian economies offer the lowest production costs, with 40 billion cubic meters available at less than USD 10/GJ, a level that is directly competitive with LNG import prices in Asia, which range between USD 8 and 14/GJ.

Biogas is of particular interest: it stands at the intersection of several themes (waste recovery, circular economy, energy security, rural development) and offers a direct substitute for natural gas without requiring new infrastructure.

IVO Capital Partners’ Positioning

IVO Capital Partners has positioned itself in this energy transition momentum in emerging markets, with EUR 225 million of bonds issued by renewable energy producers in its portfolio, half of which are issued by Indian companies, including Greenko, one of the private leaders of India’s energy transition with more than 11 GW of installed capacity, contributing concretely to the transformation of the country’s energy system. This exposure covers a broad spectrum of technologies: the IVO EM Corporate Debt Short Duration SRI fund illustrates this approach, with the electricity and heat sector representing 16% of the allocation, 100% of which is renewable generation, including initial positions in bioenergy notably through issuers such as FS Bioenergia, a pioneer of corn ethanol in Brazil.

This exposure comes with an attractive return profile: the structurally higher cost of capital in emerging markets translates, on the bond side, into higher coupons than those offered by equivalent issuers in developed countries. Investing in the emerging energy transition is therefore not only a thematic bet, but it is also a tangible source of return for fixed-income investors.

DISCLAIMER – THIS DOCUMENT DOES NOT CONSTITUTE FINANCIAL ADVICE:

The information provided reflects the opinion of IVO Capital Partners at the date of this publication. The information contained in this document is not intended to be understood or interpreted as financial advice. It is shared for informational purposes only, does not constitute advertising, and should not be construed as a solicitation, offer, invitation, or inducement to buy or sell securities or related financial instruments in any jurisdiction. CONFIDENTIALITY NOTICE: The information herein is strictly confidential and may not be reproduced, redistributed, disclosed, or transmitted to any other person, directly or indirectly. You may not copy, reproduce, distribute, publish, display, modify, create derivative works from, transmit, or exploit this content in any manner, nor distribute any portion of it over a network, including a local network, sell or offer it for sale, or use it to construct any kind of database.