The vision of IVO Capital Partners

- ETFs: A Revolution in Investment, but Struggles to Gain Ground in the Bond Market : First introduced in 1990, Exchange-Traded Funds (ETFs) revolutionized the investment landscape by offering cost-effective access to the diversification of mutual funds, equity-like tradability, return replication, and exposure to specific asset classes. Initially focused on equities, ETFs expanded into bond products in the early 2000s, bringing the global ETF market to nearly $12 trillion in assets under management (AUM) by 2024. However, bond ETFs have struggled to gain significant market penetration, consistently representing only one-fifth of total ETF AUM.

- Structural inefficiencies limit ETF adoption in emerging market debt : In emerging market (EM) debt, only 2% of assets are managed via ETFs, highlighting their limited adoption in this asset class. Structural inefficiencies inherent in EM debt, combined with the constraints of ETFs, hinder their ability to effectively manage credit risk and generate returns. Challenges include forced exposure to large debt issuers and unattractive credit, limited access to new issuances, and liquidity constraints. Despite their appeal as a low-cost investment solution, these limitations have led ETFs to consistently underperform their benchmarks and active managers.

- The superiority of active management over emerging market debt ETFs: In the emerging market debt universe, active management strategies are proving to be a far more suitable alternative to ETFs dedicated to this asset class. They offer greater flexibility in investment choices, privileged access to yield opportunities often inaccessible to ETFs, and the specialized expertise essential for navigating complex and less efficient markets.

Source: Bloomberg and IVO Capital Partners. Emerging market bond ETFs are composed of the 20 largest sector ETFs listed on page 3. Average returns and expense ratios are market capitalization-weighted averages for ETFs and fund-size-weighted averages for active emerging market debt managers. Active managers of emerging market debt are primarily corporate debt funds and include: Abrdn SICAV I – Emerging Markets Corporate Bond Fund, Aviva Investors Emerging Markets Corporate Bond Fund, BlackRock Global Funds – Emerging Markets Corporate Bond, Edmond de Rothschild Fund – Emerging Credit Fund, Goldman Sachs Emerging Markets Corporate Bond Portfolio, JPMorgan Funds – Emerging Markets Corporate Bond Fund, Ninety One Global Strategy Fund – Emerging Markets Corporate Debt Fund, Pictet – Emerging Corporate Bonds, Vontobel Fund – Emerging Markets Corporate Bond, and IVO Emerging Markets Corporate Debt. Data as of January 16, 2025.

Introduction

At IVO Capital Partners, as an asset manager specializing in EM debt, we are observing an interesting dynamic: while this asset class continues to attract investors who favor an active management approach, the initial appeal of ETFs compared to active strategies remains strong for investors new to this area or seeking alternatives. In principle, ETFs are designed to offer low-cost exposure to specific asset classes. While their advantages may seem attractive at first glance, these instruments come with significant trade-offs, particularly in the area of bonds and more specifically in emerging market debt.

Our in-depth analysis of passive and active EM debt ETFs reveals that these vehicles often fail to achieve their stated objectives, making them less effective than actively managed funds for investors seeking access to emerging debt markets.

In this note, we highlight the key limitations of EM debt ETFs (focusing primarily on passive ETFs, as active ETFs represent only a small segment of the market) and present evidence supporting our view that they are not a suitable tool for effectively accessing emerging market debt. Furthermore, we demonstrate why active management, which is central to IVO Capital Partners’ investment approach, remains a highly effective strategy for generating alpha compared to ETFs, particularly in complex and specialized asset classes.

A lack of enthusiasm for ETFs in the bond sector

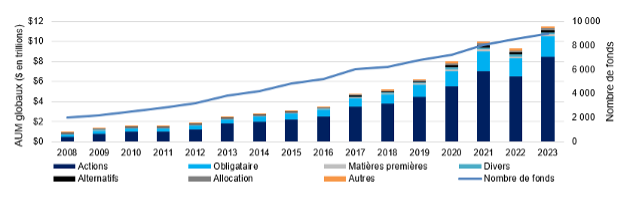

ETFs emerged in the 1990s and were designed to combine the diversification benefits of mutual funds with the tradability of stocks, while offering low-cost access to various asset classes. This financial innovation quickly gained popularity. According to Morningstar , the global ETF market is now valued at approximately $12 trillion (2024).

Initially focused on equities, the market expanded in the early 2000s to include bond ETFs, which represented $1.7 trillion in net assets by the end of 2024. These products have transformed bond investing by offering transparent, liquid, and cost-effective access to diversified bond portfolios. These ETFs appeal to investors seeking income, stability, and flexibility. Morningstar reports that, in the United States alone, ETFs and passive strategies accounted for 60% of third-party managed equity assets in 2024, compared to just 20% in 2011.

However, despite their touted advantages, bond ETFs have struggled to capture a larger market share, consistently representing only one-fifth of total ETF assets under management. Furthermore, in emerging market debt, ETFs accounted for just 2.5% of the overall market size, estimated by Goldman Sachs at approximately $1.2 trillion (excluding local sovereign debt from emerging markets, which now constitutes a $7 trillion asset class).

Graph 1

The impressive growth of ETFs, primarily driven by equities, from 2008 to 2023

Source: Morningstar. Data as of December 31, 2024.

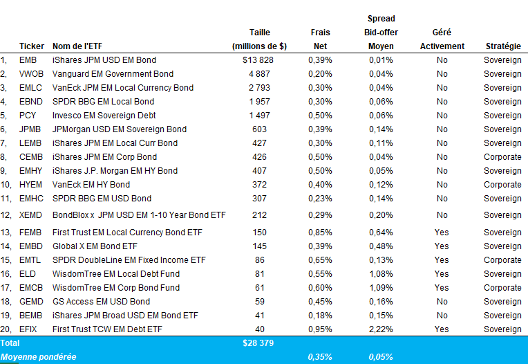

The lack of investor interest is reflected in the current limited and insufficient supply of emerging market debt ETFs (see Chart 2). Approximately 50% of assets under management in EM debt ETFs are concentrated in a single vehicle. The five largest ETFs (each managing over $1 billion) charge what we consider relatively high fees, ranging from 20 to 50 basis points, and focus primarily on sovereign debt. Active EM debt ETFs represent only 2% of total assets, or approximately $600 million. Their limited adoption is due to several factors, including higher fees (averaging 0.64%) and wider bid/ask spreads, reaching nearly 0.75%, compared to less than 0.1% for the leading passive ETFs.

Figure 2

Overview of Emerging Market Debt ETFs – Ranked by Size (in millions of dollars)

Source: Bloomberg, JP Morgan and IVO Capital Partners. Data as of December 31, 2024.

Figure 3

Profile of ETFs on Emerging Market Debt

Source: Bloomberg, JP Morgan and IVO Capital Partners. Data as of December 31, 2024.

The structural inadequacy of ETFs in the face of the specific characteristics of emerging market debt

As mentioned earlier, since their introduction in the early 2000s, the limited interest in bond ETFs, particularly in emerging market (EM) debt, highlights the persistent structural disadvantages of these financial instruments for accessing this specific market. These limitations, such as restricted investment flexibility and relatively low risk-adjusted return potential, hinder their ability to fully capitalize on market opportunities and outperform active managers.

- ETFs lack active credit risk management and are heavily exposed to large debt issuers

Passive ETFs, which represent the vast majority of EM debt ETFs, hold bonds without active analysis or risk assessment, generally holding a bond until its default. The main factor determining an issuer’s weighting in an index is its size, although there is no strong correlation between a company’s size and its default risk.

A notable example in emerging markets is that of the Chinese real estate developer Evergrande. In 2020, Evergrande was one of the world’s largest issuers of US dollar-denominated debt, but it ultimately defaulted. This illustrates that significant weightings in indices can be exposed to default risk, highlighting why ETFs may not be suitable for the credit asset class.

This contrasts sharply with equities, where markets have increasingly adopted a “winner-takes-all” logic, with large index weightings often representing the best performance. In emerging market credit, such a trend does not exist. On the contrary, a high-yield issuer with year-on-year debt is often a red flag, as illustrated by the case of Evergrande with its $100 billion debt.

This fundamental difference is one of the reasons why we believe ETFs are not suitable for our asset class, where in-depth credit analysis and active risk management are essential to navigate risks and identify attractive investment opportunities.

- ETFs are heavily exposed to unattractive loans with questionable risk-return dynamics

A notable example is Taiwan Semiconductor Manufacturing Company (TSMC), the largest holding in the JP Morgan CEMBI BD Index (2.57%). Based in Taiwan, this company currently offers an average spread of less than 50 basis points over US Treasuries. After accounting for ETF fees, the yield is equivalent to that of Treasuries, providing little to no added value. Furthermore, while TSMC is one of the index’s top-rated companies, it carries significant geopolitical risk.

This situation is reminiscent of lessons learned from past events in this asset class. For example, at the end of 2021, Russian issuers represented approximately 2.5% of the CEMBI BD index, with an average spread of 253 basis points, below the index average of 318 basis points at the time. Following the war and sanctions, Russian bonds were removed from the index with a zero valuation, resulting in significant losses for ETF investors.

In contrast, our flagship fund, the IVO EM Corporate Debt fund, had no exposure to Russia, as we had assessed its risk-return profile and determined that it offered limited potential while presenting significant risks. This ability to exercise geographic flexibility is, in our view, essential for creating additional value and navigating effectively through today’s heightened geopolitical uncertainties—particularly in light of shifting global dynamics, such as the return of Donald Trump to the US presidency.

- ETFs do not have access to the “new issue premium”

Another potential source of alpha that ETFs miss is the “new issue premium” available in the primary bond market, accessible only to active managers. ETFs cannot participate in primary markets, where newly issued bonds or debt securities are sold directly by issuers. This limitation prevents ETFs from incorporating the latest and potentially attractive investment opportunities into their portfolios.

New primary issuances often offer attractive investments thanks to the “new issue premium,” which can include higher yields, better terms, or improved credit profiles compared to existing bonds. By not having access to these opportunities, emerging market debt ETFs miss out on the chance to capture these potentially higher returns, resulting in suboptimal portfolio performance.

IVO Capital Partners’ funds, on the other hand, actively participate in the primary market, capitalizing on new investment opportunities while strengthening existing portfolio positions. Our investment team conducts ongoing reviews of new primary issues from both established and emerging issuers. In addition to our strong, long-standing relationships with issuing banks, the size of our funds, including the

- The inefficient mechanisms of ETFs for navigating less liquid markets

The creation and redemption process, central to the functioning of ETFs and essential for aligning their market price with their net asset value (NAV), is fundamentally unsuitable for accessing bond markets, particularly emerging market corporate debt (see Appendix A). This is due to the lower liquidity, reduced efficiency, and increased fragmentation of these markets.

Unlike equities, where each issuer is represented by a single principal security, bond markets include multiple instruments per issuer. For example, the JP Morgan CEMBI BD index comprises approximately 750 issuers, but more than 1,800 securities. This fragmentation can significantly impact liquidity, particularly during periods of market stress.

While mutual fund investors can trade at NAV daily, ETF investors can face significant discounts. Bloomberg reported that during the COVID-19 crisis, bond ETFs traded at impressive discounts to their NAV, which some have called a “fatal loop of illiquidity”: in 2020, approximately 70 bond ETFs traded at discounts exceeding 5% of their NAV, and 16 experienced discounts exceeding 10%. This highlights the significant costs associated with seeking liquidity during periods of crisis and market disruption.

Disappointing performance confirms the shortcomings of ETFs in accessing emerging market debt.

Due to the main structural constraints mentioned above, emerging market debt ETFs have consistently underperformed both relative to their benchmark indices and to active managers specializing in EM debt over the long term.

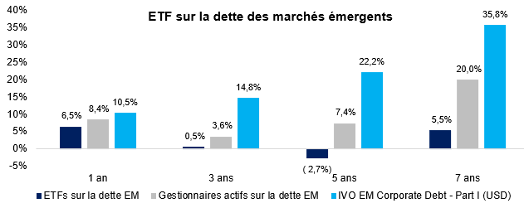

- Underperforming compared to EM indices/benchmarks

Figure 4

Average cumulative returns of emerging market debt ETFs compared to EM indices/benchmarks (in USD)

Source: Bloomberg and IVO Capital Partners. Emerging market bond ETFs are comprised of the top 20 sector ETFs listed on page 3. Average returns and expense ratios are market capitalization-weighted averages. The Bloomberg Emerging Markets Hard Currency Aggregate Index is a leading benchmark for emerging market hard currency bonds, including USD-denominated bonds issued by emerging market sovereign, quasi-sovereign, and corporate issuers. The Bloomberg EM USD Aggregate: Sovereign Index tracks fixed-rate and floating-rate US dollar-denominated bonds issued by emerging market governments. Data as of January 16, 2025.

ETFs were initially designed to offer investors low-cost access to specific asset classes, with the aim of closely replicating the returns of their underlying assets. However, as Chart 4 shows, emerging market debt ETFs have not lived up to this promise. Over several periods, they have consistently underperformed their EM bond benchmarks, calling into question their effectiveness in delivering economic returns similar to those of the benchmarks.

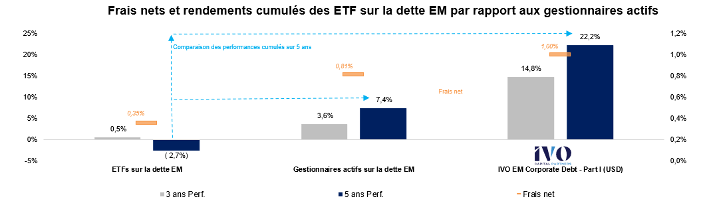

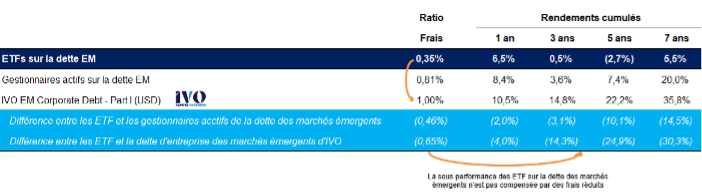

- Emerging market debt ETF: Low costs, but limited value

Figure 5

Average cumulative returns of emerging market debt ETFs compared to active managers (in USD)

Source: Bloomberg and IVO Capital Partners. Emerging market bond ETFs are composed of the 20 largest sector ETFs listed on page 3. Average returns and expense ratios are market capitalization-weighted averages for ETFs and fund-size-weighted averages for active emerging market debt managers. Active managers of emerging market debt are primarily corporate debt funds and include: Abrdn SICAV I – Emerging Markets Corporate Bond Fund, Aviva Investors Emerging Markets Corporate Bond Fund, BlackRock Global Funds – Emerging Markets Corporate Bond, Edmond de Rothschild Fund – Emerging Credit Fund, Goldman Sachs Emerging Markets Corporate Bond Portfolio, JPMorgan Funds – Emerging Markets Corporate Bond Fund, Ninety One Global Strategy Fund – Emerging Markets Corporate Debt Fund, Pictet – Emerging Corporate Bonds, Vontobel Fund – Emerging Markets Corporate Bond, and IVO Emerging Markets Corporate Debt. Data as of January 16, 2025.

One of the main arguments in favor of ETFs for investors is their cost-effectiveness. According to our analysis, the average expense ratio for all emerging market debt ETFs, whether passive or active, is 35 basis points, compared to 80 basis points for actively managed EM debt funds. While ETFs are generally (slightly) less expensive, this cost advantage becomes negligible when considering the historical returns of active managers.

As illustrated in Chart 5, active managers of EM debt, including the IVO EM Corporate Debt fund, have consistently outperformed ETFs over several periods. Over a five-year period, the average investor in an EM debt ETF would have saved 65 basis points per year in fees compared to our IVO fund, but would have lost 25% in cumulative performance. This consistent outperformance clearly demonstrates that the cost savings offered by ETFs do not offset the value generated by active management with higher fees.

Conclusion

While ETFs have gained popularity as a cost-effective way to access various asset classes, such as equities, they struggle to gain traction in the bond market due to significant structural weaknesses. Our in-depth analysis of the EM debt ETF market reveals that these vehicles, whether passive or active, are ill-suited to navigating less liquid, less efficient, and more complex markets like emerging market debt.

Their promise of lower costs does not offset their consistent underperformance relative to benchmark indices and comparable active managers. Furthermore, ETFs have significant disadvantages compared to actively managed funds, such as the IVO EM Corporate Debt fund. Leveraging our experienced investment team, a robust fundamental research framework, deep local expertise, advanced analytical tools, and active risk management, we are better equipped to manage risk, capitalize on investment opportunities, and generate alpha in the EM debt markets.

IVO Capital Partners Focus

At IVO Capital Partners , we are convinced that the superiority of active management over ETFs in emerging market debt underlines the essential role of the “human” factor in navigating opaque and less efficient markets.

Our investment team consists of 4 portfolio managers, 7 analysts including an ESG specialist and 1 trader dedicated to execution.

Our team of credit analysts is responsible for identifying, researching, and evaluating investment opportunities in credit-related securities, following a rigorous fundamental research process that reflects our investment philosophy and has been refined over the years. Our analytical coverage is based on a sector and geographic model, enabling us to effectively leverage in-depth expertise. Given the diversity of our investment universe, spanning multiple geographic regions, local knowledge is crucial for identifying and managing opportunities across a wide range of jurisdictions.

In addition to English and French, several team members are fluent in Spanish, Portuguese, and Mandarin, which allows us to incorporate local perspectives, navigate regional regulations, and engage directly with corporate leadership teams.

Given the relative illiquidity of emerging market bonds, high-quality trade execution is a critical component of our investment process in this asset class. The ability to efficiently source bond liquidity at any time is paramount. Our dedicated and experienced execution desk enables us to leverage our high-quality fundamental analysis through responsive, best-in-class execution strategies via a broad network of counterparties.

Furthermore, the recent resurgence of the new issues market has reinforced the importance of this network in our strategy. In addition to our strong, long-standing relationships with issuing banks, the size of our funds, including the IVO EM Corporate Debt fund with €800 million in assets under management, allows us to secure preferential allocations to new issues at attractive prices, offering upside potential. This strategic advantage enables us to generate alpha and deliver superior performance.

In conclusion , we believe that the structure and expertise of our investment team, combined with a rigorous fundamental research process, ideally position us to effectively identify new opportunities, manage risks and generate alpha in emerging market corporate debt.

DISCLAIMER: THIS DOCUMENT DOES NOT CONSTITUTE FINANCIAL ADVICE. The information contained in this document is not intended to be understood or construed as financial advice. It has been shared for informational purposes only, does not constitute advertising, and should not be construed as a solicitation, offer, invitation, or inducement to buy or sell securities or related financial instruments in any jurisdiction. CONFIDENTIALITY: This information is strictly confidential and may not be reproduced, redistributed, disclosed, or transmitted to any other person, directly or indirectly. You may not copy, reproduce, distribute, publish, display, perform, modify, create derivative works from, transmit, or otherwise exploit such content, nor distribute any portion of this content over any network, including a local area network, sell or offer it for sale, or use this content to construct any type of database.

IVO Capital Partners │Simplified joint-stock company with capital of €250,000 Registered office │ 61-63 Rue des Belles Feuilles, 75016 Paris │ 753 107 432 000 35 RCS Paris │VAT No.: FR 54 753107432

Annex A

Back to basics

Understanding the ETF trading mechanism is essential, as there are notable limitations regarding bond ETFs, particularly those involving less liquid securities, such as emerging market corporate bonds.

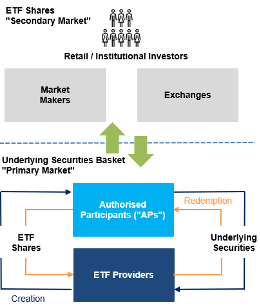

At the heart of how an ETF works is the creation/redemption process, a mechanism designed to align the ETF’s market price with its net asset value (NAV) (see Figure 6 below). This process involves authorized participants (APs)—large financial institutions such as Citadel Securities, Jane Street, and Flow Traders—acting as intermediaries. During the creation process, PAs provide the issuer with a basket of bonds reflecting the ETF’s assets in exchange for new ETF units. These units are then sold on the market to meet investor demand and prevent the price from exceeding the NAV. Conversely, during the redemption process, PAs buy ETF units on the market and return them to the issuer in exchange for the underlying bonds, thereby reducing the supply of units and bringing the price back in line with the NAV.

Figure 6

Creation/Redemption Process

Source: IVO Capital and Financial Times.

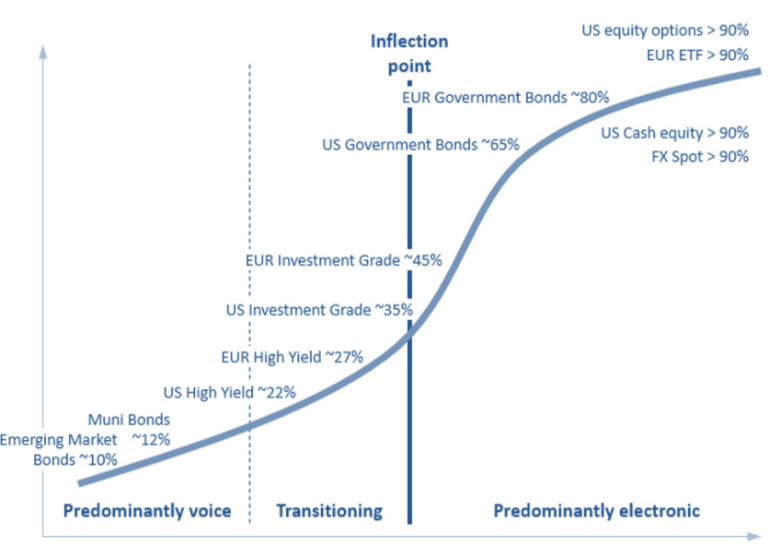

Figure 7

EM bonds are traded by voice. An image containing text, diagram, line, plot. Automatically generated description.

Source: Flow Traders Data (2023).

This process, typically carried out in kind (using securities rather than cash), improves liquidity and helps minimize costs, even in less liquid bond markets. However, the liquidity of the underlying bonds remains a critical factor. Bond securities, particularly high-yield (HY) or emerging market bonds, often exhibit lower liquidity, complicating the creation and redemption process. For example, bid-ask spreads on emerging market corporate bonds can exceed 2 basis points.

A key technical reason for the success of ETFs in equity markets and more liquid bond segments (such as government bond markets) is the widespread “electronification” of trading in these asset classes. As illustrated in Figure 7, the majority of transactions in equity products and major government bonds are now conducted electronically.

In contrast, other segments of the credit markets, such as emerging market bonds, are still predominantly (90%) traded via voice or messaging. This manual trading process plays a crucial role, allowing human traders within active asset managers to negotiate bid-ask spreads more effectively than those initially offered by brokers. Therefore, the lack of electronic trading in emerging market bonds significantly hinders the automation of the ETF creation process, making it more complex, inefficient, and slow.

As a result, ETFs that track indices composed of less liquid securities, such as emerging market corporate bonds, are subject to still inefficient trading mechanisms and discrepancies between their NAV and their market price — inherent limitations already explored in this note.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}