Emerging countries, the designated culprits of climate change?

A biased view of the global energy transition

Mathieu Quenechdu, ESG analyst at IVO Capital Partners

The vision of IVO Capital Partners

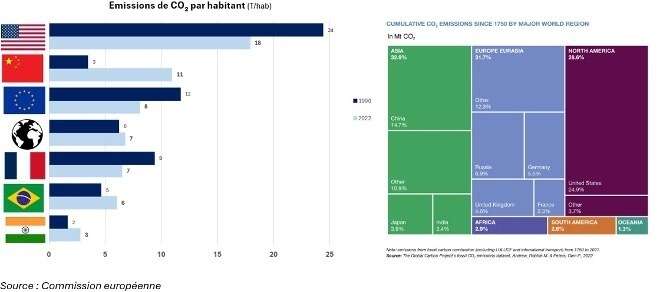

- For several years, emerging countries have been accused of being the main emitters of greenhouse gases.

- (GES). A reading in absolute value reinforces this image, obscuring several realities.

- On the one hand, developed countries have historically been the main beneficiaries of fossil fuels and those that have contributed the most to GHG emissions. On the other hand, per capita emissions remain much higher in the United States and Europe (excluding China).

- One of the key challenges of the COPs is to direct capital to these economies to accelerate their transition. However, these countries face a double bind: facing the effects of climate change while lacking the resources to respond.

Thus, far from being inactive, emerging countries are deploying ambitious policies to green their energy mix.

An emerging market conducive to sustainable investment

Sustainable investment in emerging countries is often perceived as limited due to a lack of sufficiently green alternatives. However, this reasoning is flawed: emerging countries are experiencing a changing energy mix and a decarbonization of electricity. The electricity and heat sector is the world’s leading source of GHG emissions, but also the one where the transition is most accessible thanks to existing technologies (solar, wind, hydroelectric, etc.).

Some emerging countries are already establishing themselves as key players in this transformation. In Latin America, more than 50% of electricity generation comes from renewable energy. Replacing carbon-intensive energy sources with renewable energy has a significant direct impact. A good number of emerging countries are making a name for themselves in this transition, particularly in Asia. For example, India is accelerating its transition with an ambitious investment plan of USD 13.3 billion by 2024 (+40

% in one year, Ember, Navigating risks to unlock 500 GW of renewables by 2030, February 2025 ) to diversify its energy mix and thus reduce its dependence on coal. Investing in renewable energy amounts to a trade-off against coal and gas, resulting in a net reduction in emissions – 665 times and 98 times respectively, for equivalent generation – by redirecting capital towards lower-carbon solutions.

Furthermore, the emerging world is experiencing energy expansion, with a growing need for access to electricity to support its growth and develop its infrastructure. Indeed, 80% of the world’s additional electricity demand by 2030 will come from emerging countries. It is necessary to supply this surplus with low-carbon (renewable) energy and limit the environmental impact of this energy expansion.

Thus, emerging countries play a key role in the energy transition, with players such as Latin America, where a large share of electricity already comes from renewable sources, and India, which is actively building its transition and its additional energy demand thanks to massive investments in clean energy.

ESG reporting aligned with international standards:

Contrary to popular belief, the lack of transparency among emerging companies is becoming less of a problem. While ESG disclosure requirements are increasingly being challenged in developed countries—with the Trump administration, hostile to ESG, or the Omnibus Law in the EU—emerging countries are increasingly aligning their requirements for disclosing companies’ environmental and social impacts with international standards. In Brazil, the Brazilian Securities Commission issued a resolution requiring publicly listed companies to comply with the IFRS (ISSB) sustainability standards. Mexico, for its part, has imposed the same requirement starting in January 2025 on companies listed on its markets. Similarly, Colombia developed its own green taxonomy within its legal framework in 2022, detailing the criteria for issuing green and sustainable bonds.

In reality, emerging countries have no shortage of sustainable investment opportunities, and emerging market institutions are implementing regulatory frameworks conducive to sustainable investment. So, what are the dynamics of sustainable investment in emerging countries?

Investment Gap in EM: Stimulating International Finance for a Sustainable Global Energy Transition

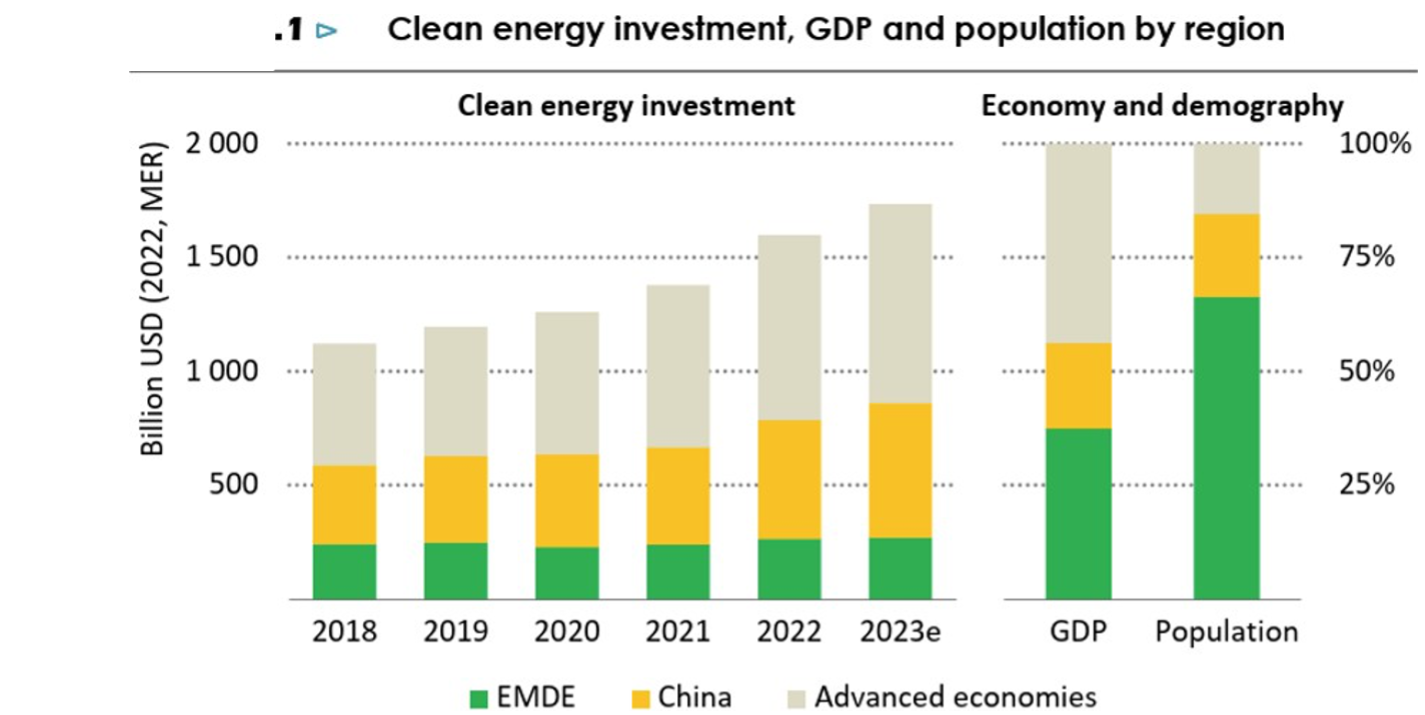

The latest report from the International Energy Agency (IEA) highlights the lack of investment in clean energy for emerging economies. Currently, these countries attract less than 20% of global investment in this sector, despite the fact that they represent nearly two-thirds of the world’s population and a growing share of energy demand.

Faced with insufficient local financing, it is necessary to strengthen international financing with the objective of tripling it by 2035. Public actors, such as Development Finance Institutions (DFIs) like the World Bank and the African Development Bank, play a key role. However, private actors and capital markets are also essential.

In this sense, there is a strong growth in green bonds in emerging markets, with a 50% increase between 2022 and 2023, now representing 40% of the global primary green bond market in 2023, but these amounts are still not sufficient ( World Investment report 2024 – UNCTAD ).

So what are the obstacles to attracting more investment?

A high cost of capital: a barrier or an investment opportunity?

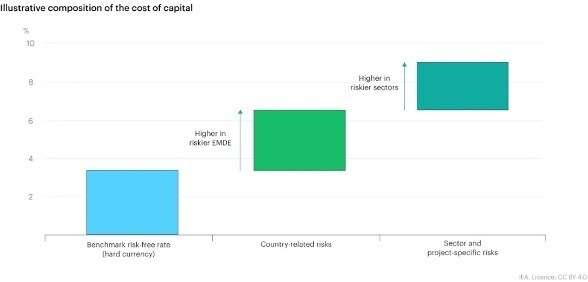

Today, the main obstacle to sustainable investment in emerging markets is the cost of capital (WACC). The cost of capital reflects the return on investment expected by shareholders and creditors. This cost is higher in emerging markets than in developed countries.

Source: International Energy Agency

Indeed, investors demand a yield premium to finance companies operating in emerging economies, due to the specific risks associated with these markets (currencies, politics, regulations, etc.). This requirement slows the inflow of investments. In addition, the credit rating of these companies, often classified as “high yield,” reduces their attractiveness to new investors.

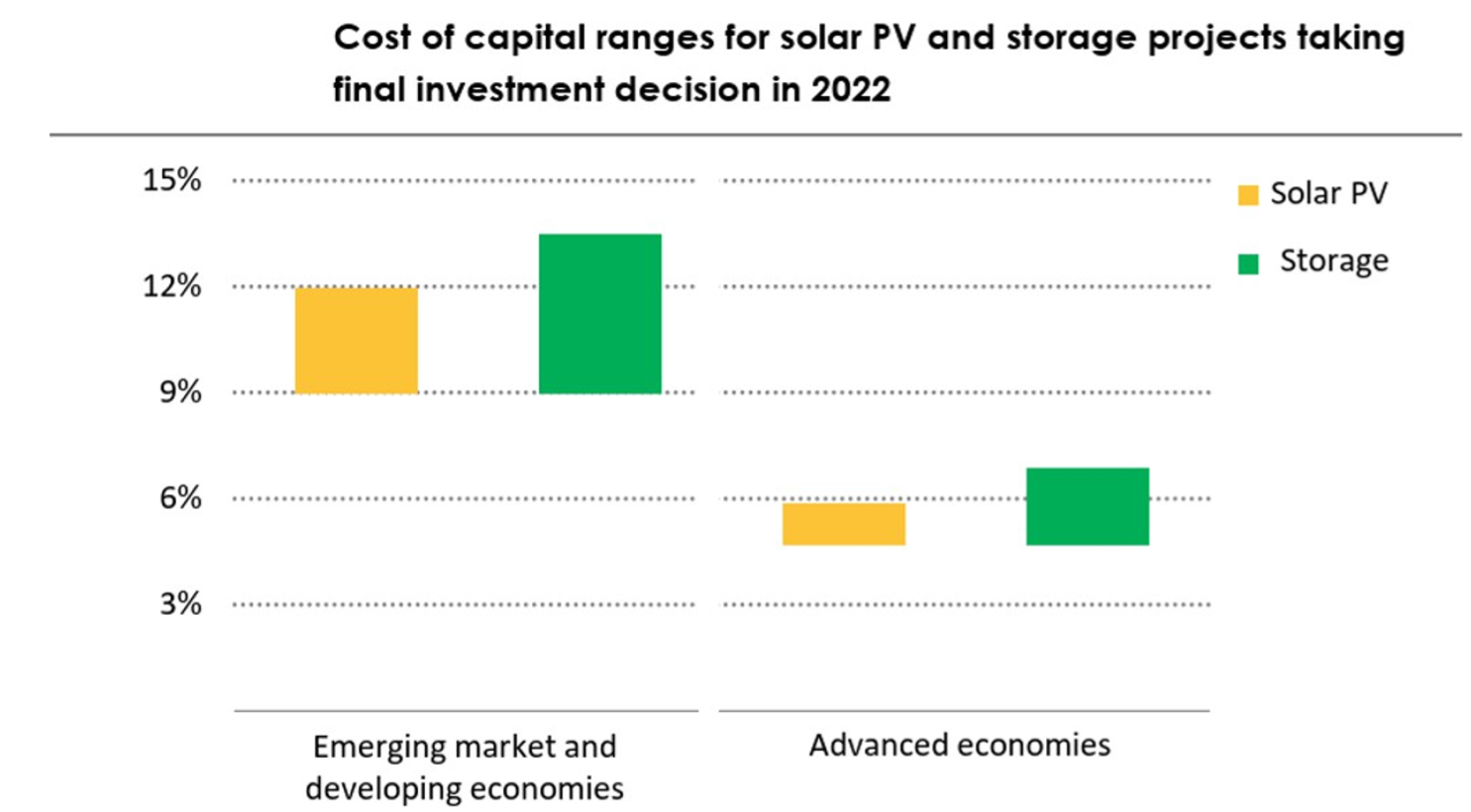

For example, if we take a solar energy project, this cost can be up to twice as high as in developed countries for an equivalent project. Note that the capital cost of a solar project is mainly borne by debt (65% on average).

Source: International Energy Agency

Thus, the cost of capital hinders the dynamics of project financing despite a real need. Indeed, a reduction in this cost would alleviate the annual financing needs of emerging countries (-100 basis points would be equivalent to approximately $150 billion less each year) and thus facilitate the achievement of energy transition objectives.

It is true that a high cost of capital reflects a higher risk premium. However, it also represents an attractive investment opportunity for investors seeking higher returns.

Indeed, navigating the emerging universe requires expertise and a detailed (“bottom up”) analysis of the quality of issuers

and the means they implement in the face of identified risks.

For over 13 years, IVO Capital Partners has been analyzing these opportunities in emerging markets.

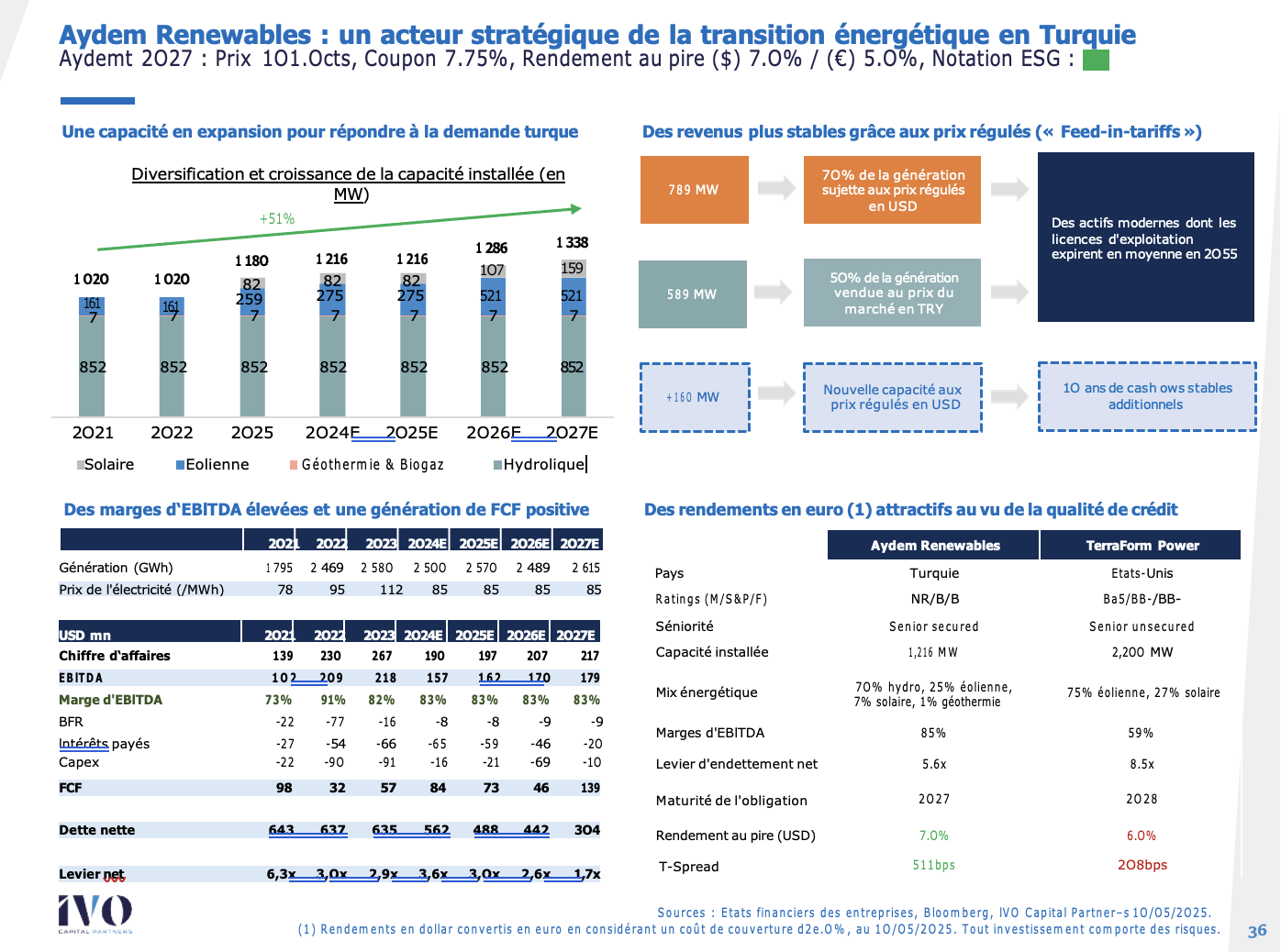

Investment case of a renewable electricity generation company in Türkiye: Aydem Renewables

Turkey’s energy mix is still dominated by fossil fuels, which account for 60% of total production, 36% of which comes from coal.

However, renewable energy accounts for 40% of the mix, with significant growth in recent years. Historically focused on hydropower, Turkey is now seeking to exploit its wind and solar potential by quadrupling their installed capacity, with the goal of reaching 120 GW by 2035 ( Reuters, Turkey aims to quadruple wind and solar energy capacity by 2035 ) .

Source: International Energy Agency

Aydem Renewables is part of this dynamic. Aydem is a recent player with limited size (1.2 GW / 1% market share) and little track record on the operational quality of its assets. Present only on the Turkish market, Aydem is originally a hydroelectricity specialist. The company is now expanding its portfolio by developing solar and wind production capacities.

Aydem issued a dollar bond maturing in 2027, with a B credit rating, a coupon of 7.75% and a debt leverage of 6.3x when it was issued on July 19, 2021. At first glance, these elements could deter some investors.

However, several creditor protection mechanisms can reduce the risk associated with high leverage.

time of broadcast.

Aydem plays a strategic role at the heart of the energy transition in Türkiye, relying on several assets:

- Essential assets for the State, both tangible and strategic.

- Project Bond financing, secured by core operating assets, with an amortizing structure that gradually reduces debt leverage. This offers strong credit benefits for bondholders, limiting refinancing risk and protecting against impairment.

- Protective covenants , including strict supervision of the dividend policy to preserve the bond’s repayment capacity.

- Stable electricity prices indexed to the dollar thanks to the Feed-in-Tariff mechanism for renewable energy in Turkey, reducing exposure to the risk of depreciation of the Turkish lira.

- A high EBITDA margin that ensures robust profitability and contributes to strengthening the issuer’s credit profile.

Aydem offers an attractive risk/return ratio and a structurally advantageous bond for creditors. Indeed, this company suffers from the poor quality of Turkey’s sovereign rating (B+), which impacts its cost of credit. Its “zip code” imposes a credit risk premium 1.5 times higher (311 bps vs. 208 bps) compared to an equivalent project in the United States, despite a debt leverage 2.5 times lower. Today, the Aydem 2027 bond offers an attractive yield of 7% in USD (5% in EUR), in line with our investment philosophy: “Bad country / Good society.” In addition, Aydem 2027 is a green bond, aligned with international sustainability standards and compliant with the investment definition of the European Taxonomy.

This case illustrates the challenges and opportunities of financing the energy transition in emerging countries, where credit risk remains a key factor.

Conclusion

The need for financing in emerging markets is clear, and opportunities exist for sustainable impact investing. However, this momentum is hampered by the high cost of capital inherent in emerging markets. Yet, financing sustainable development in these regions also represents an opportunity to take advantage of long-term investment trends in strategic infrastructure, which have historically offered greater return visibility and stability for credit investors compared to more cyclical industries.

IVO Capital Partners has been investing in emerging markets for over 13 years, with extensive experience in this sector through a team of 11 people.

The IVO EM Corporate Debt Short Duration SRI fund is part of this dynamic by sustainably financing companies operating in emerging markets while seizing investment opportunities offering attractive returns. Currently, the electricity and heat sector represents 20% of the allocation (in 6 countries), with 100% renewable generation and a yield of 7.3% in USD as of 28/02/2025.

DISCLAIMER THIS DOCUMENT DOES NOT CONSTITUTE FINANCIAL ADVICE:

The information communicated reflects the opinion of IVO Capital Partners as of the date of this publication. The information contained in this document is not intended to be understood or interpreted as financial advice. It has been shared solely for informational purposes, it does not constitute an advertisement and should not be construed as a solicitation, offer, invitation, or inducement to buy or sell securities or related financial instruments in any jurisdiction. CONFIDENTIALITY: The information is strictly confidential and may not be reproduced, redistributed, disclosed, or transmitted to any other person, directly or indirectly. You may not copy, reproduce, distribute, publish, display, perform, modify, create derivative works from, transmit, or in any way exploit any such content, nor distribute any part of this content over any network, including a local area network, sell or offer it for sale, or use this content to build any type of database.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}